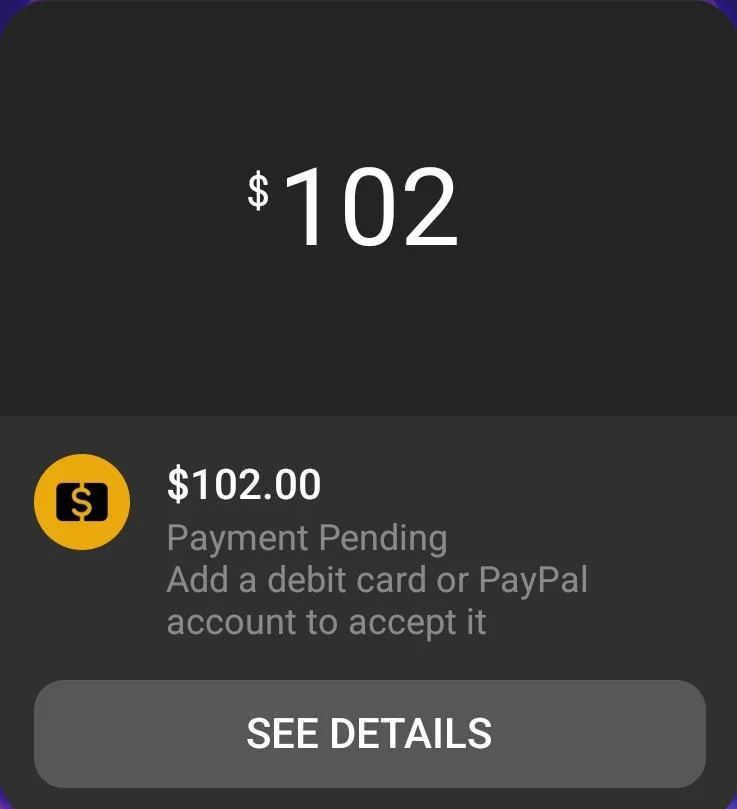

Facebook messenger payment pending

A prolonged facebook messenger payment pending status can cause sales agreements to stall and affect the credibility of the parties involved. Typically, the system needs time to verify the security of the funds or check the compatibility between the issuing bank and Meta’s risk filters. To avoid confusion when encountering this display error, users need to clearly distinguish between system delays and errors from the card service provider. Let’s join RentAds in exploring the potential causes behind the facebook messenger payment pending notification and the necessary verification steps to release the cash flow as quickly as possible

The Root Causes of Cash Flow Bottlenecks When facebook messenger payment pending

A stalled money transfer is not merely a display glitch, but the consequence of technical conflicts between the platform and financial institutions. When the balance has been deducted but the destination wallet has not received the funds, the transaction is effectively stuck at Meta Pay’s risk-control checkpoints. This phenomenon reflects the complexity involved in synchronizing data between international payment servers and local transaction management systems. Breakdowns in information flow often occur when Meta’s multilayered security mechanisms detect incompatibilities, prompting a temporary freeze of funds to allow in-depth post-transaction verification, including checks related to facebook money transfer fee structures and settlement logic.

Algorithm for Screening Abnormal Transactions

The system automatically scans transfer orders based on historical spending behavior. Payments with suddenly large values or initiated from unfamiliar geographic locations are temporarily held for verification, in order to mitigate risks of money laundering and digital asset misappropriation. Meta Pay’s algorithms operate on machine learning models that continuously update variables related to user habits. Any abrupt change in login device or the execution of a transfer far exceeding the average monthly spending threshold will immediately trigger a pause mechanism.

Evidence of this process can be observed in the fact that cross-border transfers often require longer processing times than domestic transactions, as they must pass through additional filters related to counter-terrorism financing and compliance with international financial regulations. Accounts with infrequent transaction histories that suddenly initiate transfers worth thousands of USD are typically suspended by the system, pending two-factor authentication or manual review by risk specialists before funds are ultimately released.

Reconciliation Barriers Between Linked Banks

Time discrepancies in update cycles between Meta’s payment gateway and domestic banking systems frequently generate delays. Transactions executed during system maintenance windows or over weekends are especially prone to being placed in a “pending” state, awaiting manual reconciliation by technical staff. When Meta issues a debit request, the card-issuing bank must confirm the account’s validity. If the bank’s response is delayed due to unstable network infrastructure or routine core-system scans, the transaction is pushed into a pending state to prevent duplicate charges or balance inconsistencies.

In practice, there is a marked disparity in processing speed between banks that have adopted modern SWIFT systems and those still operating with incomplete digital infrastructure. Transactions initiated on Friday evenings in U.S. time zones often remain stuck until the first business day of the following week, as financial institutions require time to reconcile massive transaction datasets accumulated over the weekend. The absence of real-time API connections between Meta and certain smaller banks further exacerbates these cash flow bottlenecks.

Escrow Mode for Temporary Fund Retention

For purchase transactions, Facebook activates a temporary fund-holding mechanism to protect buyers. Funds are only fully released after delivery confirmation or the expiration of the dispute window, thereby reducing fraud risks in direct commerce conducted via Messenger. This is a third-party intermediary transaction model in which money is not transferred directly to the seller’s wallet but stored in a secure Meta-controlled escrow environment. The mechanism safeguards consumers against scenarios where sellers receive payment without delivering goods or deliver items that do not match descriptions.

The most prominent examples are transactions conducted through the “Checkout” feature on Facebook Marketplace or Messenger in developed markets. When buyers click the payment button, the system debits the card but shows a “pending” status to the recipient. The escrow period typically ranges from three to seven days, or longer depending on the shipping status provided by partnered logistics services. The retention of funds is Meta’s most powerful tool for enforcing commercial quality on the platform, compelling merchants to strictly honor service commitments before they can access their revenue.

Roadmap for Releasing Funds Stuck in the System

To end an indefinite pending state, users must intervene through technical measures and direct verification procedures with financial administration teams. Proactively engaging with Meta Pay’s operational processes not only restores cash flow but also reestablishes the account’s financial credibility. Rather than passively waiting for automated algorithmic responses, a structured intervention roadmap from entity transparency to resolving technical barriers can deliver immediate settlement outcomes.

Standardizing Payment Account Identification (KYC)

Providing complete identification documents and biometric verification helps an account exit the “suspicious” category. A clean profile enables future payments to pass Meta’s security filters quickly without requiring manual post-review. In digital finance ecosystems, KYC functions as the ultimate “passport,” allowing systems to distinguish legitimate transactions from fraudulent behavior. Once an account completes identity verification using digitized passports or national ID cards, its trust score increases sharply, significantly reducing the likelihood of funds being held by AI algorithms for risk assessment.

Real-world data shows that verified accounts experience up to 70% fewer “pending” transactions compared to anonymous or sparsely documented accounts. When cash flow disruptions occur, an approved KYC profile becomes the priority basis for Meta’s financial specialists to accelerate manual reviews, as the transacting entity has already been legally and systemically validated for transparency.

Retrieving the Transaction Approval Code

Contacting the bank’s hotline to obtain the unique transaction identifier is critical. Using this code when submitting a support request to Facebook establishes a solid legal and technical basis, enabling Meta to trace the transaction and expedite settlement into the receiving wallet. The approval code (typically a six-digit number) is the most crucial technical proof that the bank has authorized the release of funds. When transactions become stuck, the issue often lies in confirmation data failing to reach Meta’s servers due to protocol or connectivity errors.

Possessing this code gives users a decisive advantage when working with Facebook’s technical support teams. In international financial reconciliation records, the Approval Code is regarded as the key to manual “order matching.” Once provided in a support ticket, Meta’s system can immediately query intermediary payment gateways to confirm that funds have indeed been transferred, thereby issuing a release order without waiting for the system’s automated reconciliation cycle.

Adjusting Access Methods and Cache Memory

Data synchronization errors in mobile applications frequently cause transaction statuses to fail to update. Switching to a desktop browser and clearing cache memory helps reestablish connections with payment servers, ensuring accurate reflection of actual cash flow status. Mobile apps often store local data to optimize user experience, but this can lead to discrepancies between displayed interfaces and real-time data on Meta Pay’s servers.

Accessing standard web browsers such as Chrome or Microsoft Edge creates entirely new sessions. Technical evidence shows that clearing cache and cookies removes outdated files that may contain error scripts locking the interface into a false “pending” state. Desktop access forces Meta’s servers to return the latest transaction status, allowing users to see real settlement outcomes or receive advanced error-handling instructions that mobile app versions may have inadvertently omitted.

How to Configure an Uninterrupted Payment Flow

Building a “trusted payment ecosystem” is the sustainable solution to eliminating persistent pending notifications in future transactions. An uninterrupted payment flow is essentially the result of close coordination between entity transparency, payment method reliability, and disciplined spending limit allocation.

Step 1: Prioritize Verified Credit Card Streams

Credit cards consistently receive higher processing priority than debit cards or newly created e-wallets within the Meta Pay system. Unlike debit cards, which depend entirely on available balances at scan time, credit cards represent bank-backed credit limits, sending strong trust signals to Facebook’s risk filters. Using highly reliable funding sources can reduce manual holds by up to 80%, as issuing banks have already conducted financial capacity assessments on cardholders on Meta’s behalf.

Step 2: Allocate Transfer Limits Strategically

Instead of consolidating large sums into a single transaction, splitting payment values optimizes instant approval rates from automated security systems. Anti–money laundering algorithms typically impose “sensitivity thresholds” on transactions exceeding the norm for personal accounts. When a high-value transfer appears suddenly, the system defaults to a “Pending” state for post-review.

Transactions below USD 500 generally achieve significantly higher instant settlement rates compared to single transactions exceeding USD 2,000. Executing transactions during the issuing bank’s business hours is also a key technical factor.

Step 3: Maintain Transaction Trust Scores

Accounts with healthy activity histories, genuine interactions, and no financial disputes are prioritized by algorithms. In such cases, most payments are processed in real time without verification barriers. Trust scores are reinforced through consistency across personal information, access geolocation, and regular financial activity. Once an entity demonstrates long-term stability, Meta Pay relaxes risk controls, allowing funds to circulate at maximum speed.

Long-standing advertising accounts can spend tens of thousands of USD per day without invoice holds, while new accounts may be blocked at their first USD 50 transaction. The difference lies in clean payment histories without chargebacks or declines due to insufficient funds.

Contact Info

We provide services google ads agency account for rent nationwide, and with a team of experienced and qualified staff who both support advertising and can directly perform Facebook advertising if you need. Contact us via phone number.

Frequently Asked Questions

Processing times can range from a few minutes to several days, depending on the payment method and required verification levels. Transactions via international cards or linked wallets typically involve more checks than domestic methods. Unusually prolonged pending statuses may indicate the need for additional verification or technical issues.

Yes. If verification fails or the payment method is rejected at the final stage, the transaction will not complete and funds will be returned to the original source according to the bank’s processing cycle. Refunds are not immediate and depend on the issuing bank or associated financial institution’s timelines.