Facebook not accepting my credit card

You have prepared a large budget and a potential campaign, but the system continuously responds that facebook not accepting my credit card, causing all plans to come to a standstill. This situation usually arises from the tightening of Meta’s security algorithms or strict international transaction control regulations from the issuing bank. Instead of repeating the card-adding actions that raise suspicion within the system, you need a standardized roadmap to re-establish payment rights. Let’s join RentAds in exploring the deep-seated reasons why facebook not accepting my credit card and the technical measures to thoroughly resolve this issue.

System Barriers Behind Facebook Not Accepting My Credit Card

Credit card rejection issues often stem from Meta’s strict security mechanisms designed to prevent cross-border financial fraud. Error notifications not only disrupt campaign delivery but also directly affect the credibility score of the advertising account manager. Any lack of synchronization between cardholder information, the bank’s security configuration, and Facebook’s error-scanning algorithms can create barriers that block access to advertising budgets, resulting in the persistent problem commonly described as Facebook not accepting my credit card.

Risk-Based Card BIN Screening Mechanism

Meta’s algorithms automatically place certain card number ranges into restricted lists if they record high rates of bad debt or payment disputes from the issuing banks. Using a card classified as “High Risk” can lead to immediate rejection of the linking request, even when the spending limit is sufficient. Every credit card contains the first six to eight digits known as the Bank Identification Number (BIN), which allows intermediary systems to identify the issuing country and bank. When a particular region or financial institution shows excessive cases of advertising debt defaults or refund abuse, Meta enforces a blanket block on that BIN range to protect system revenue streams.

Conflicts in 3D Secure Authentication Protocols

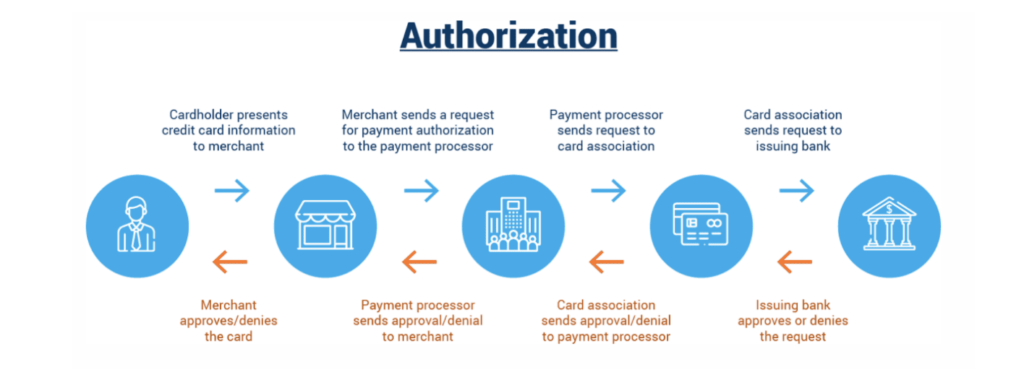

Many international credit cards require OTP-based security for every transaction, which conflicts with Facebook’s automated charging mechanism. Incompatibility between the bank’s real-time authentication requirements and Meta’s automated server-side charge requests leads to payment rejection. The 3D Secure protocol is designed to require manual user confirmation via phone or banking app at the time a transaction occurs. Facebook, however, operates on a “Pull” model, where the system proactively scans the card and withdraws funds once advertising spend reaches a threshold or an invoice cycle closes, without cardholder intervention.

This conflict creates a recurring error loop: Meta initiates a debit request, while the bank holds the transaction pending OTP confirmation. Without immediate authentication feedback, Meta’s servers log the transaction as failed and flag the card as problematic. Technical evidence shows that rejection rates rise sharply in markets with stringent payment security regulations, where issuing banks mandate multi-factor authentication for all cross-border transactions. As a result, advertisers often must contact their issuing banks to request that Meta be added to a “Whitelisted Merchant” list, allowing automated charges to bypass traditional 3D Secure protections.

International Spending Limit Constraints

Banks typically set low default thresholds for online payments to protect cardholders. If projected advertising spend exceeds these preset limits, the banking system automatically issues a decline, prompting Facebook to mark the payment method as unavailable. International spending limits operate independently of the card’s total credit limit. A cardholder may have a $10,000 credit line, but if the daily online spending cap is set at $500, any attempt by Facebook to charge larger advertising invoices will be blocked immediately as an anti-fraud precaution.

This issue most commonly arises when businesses scale their campaigns. During initial phases, small invoices are processed smoothly, but as spending increases or daily totals hit the card’s limit, repeated errors occur. This problem does not originate from Meta’s systems but is entirely due to the issuing bank’s security settings.

Process for Reinstating Credit Card Payment Authorization

Resolving card errors requires standardized financial data adjustments to rebuild trust with Meta Pay’s risk control systems. The process of reinstating payment authorization must be grounded in a clear understanding of international payment gateways and issuing bank security layers. The objective is to create a transparent transaction environment where every debit request from Meta is approved instantly, without encountering defensive barriers from financial institutions.

Activating International Payment Features

Proactively contacting the bank’s hotline or using the banking app to enable international online payments is a prerequisite for Meta’s system to accept the card. Newly issued credit cards are often locked by default for cross-border spending or restricted to domestic use to mitigate data theft risks. Without activating e-commerce transaction permissions, any connection attempt from Facebook servers located overseas will be blocked at the first security layer.

Major banks apply automated security filters to merchants headquartered abroad. Once international payment functionality is confirmed as active, the bank prioritizes authentication requests from Meta, shortening approval response times. This ensures that when Facebook scans the card, the request passes smoothly through interbank systems without being stalled due to restricted international fund access.

Ensuring Available Credit Balance

Meta typically performs temporary verification charges of at least $1 (or equivalent) to confirm card functionality. If the remaining credit limit is insufficient to cover existing advertising debt plus this verification amount, the system automatically marks the card as unavailable. Additionally, absolute accuracy in entering sensitive details—including card number, expiration date, and especially the CVV/CVC security code—is mandatory to pass payment data integrity checks. Practical records show that even minor errors in expiration dates or confusion between the digit “0” and the letter “O” in security codes can trigger Meta’s brute-force attack prevention mechanisms.

Synchronizing Billing Address and Postal Code

Billing address verification is part of the Address Verification System (AVS) used by international payment gateways to confirm card ownership. Ensuring that the postal code exactly matches the address registered with the issuing bank eliminates suspicions of stolen card usage. When Meta submits authentication requests, it includes the user-provided address data. If the bank responds that this information does not match its records, the transaction is rejected for security reasons. In strict markets such as the United States or Europe, even a minor ZIP code mismatch can cause immediate payment failure, despite sufficient credit availability.

Switching to a Backup Payment Method

In some cases, a bank’s internal anti-fraud systems automatically flag transactions from “Facebook” due to high-frequency charges. If all technical interventions fail within 24–48 hours, the definitive solution is to switch to a card issued by another bank with higher credibility or better compatibility with Meta’s ecosystem.

Certain banks achieve significantly higher international approval rates by investing in API infrastructure that connects directly with major merchants. Using a backup card from a different financial institution not only allows campaigns to continue operating but also helps determine whether the issue lies in the original bank’s policies or within Meta’s account configuration. Flexibility in managing multiple payment methods is the key to maintaining stable cash flow under fluctuating technical conditions.

Contact Info

We provide services google ads account for rent nationwide, and with a team of experienced and qualified staff who both support advertising and can directly perform Facebook advertising if you need. Contact us via phone number.

Frequently Asked Questions

Rather than focusing solely on the card, users should evaluate the entire ecosystem, including the advertising account, payment methods, transaction history, and policy compliance levels. A synchronized review of these factors helps identify root causes and select appropriate solutions, avoiding repeated card testing that may trigger additional system warnings.

Potentially, yes. When budgets are fragmented across multiple campaigns, sub-accounts, or pages simultaneously, Facebook aggregates incurred charges for payment processing. If spending patterns become unpredictable, the system tends to tighten payment controls, resulting in card rejection even when total spend is modest. This scenario commonly affects agencies or accounts managing multiple parallel campaigns.